An Unbiased View of Mortgage Investment Corporation

An Unbiased View of Mortgage Investment Corporation

Blog Article

How Mortgage Investment Corporation can Save You Time, Stress, and Money.

Table of ContentsThe Ultimate Guide To Mortgage Investment CorporationAn Unbiased View of Mortgage Investment CorporationThe smart Trick of Mortgage Investment Corporation That Nobody is Talking AboutMortgage Investment Corporation for DummiesThe Definitive Guide to Mortgage Investment Corporation

Does the MICs credit history committee testimonial each mortgage? In many circumstances, home mortgage brokers handle MICs. The broker needs to not serve as a participant of the credit committee, as this puts him/her in a direct conflict of rate of interest considered that brokers usually gain a commission for placing the mortgages. 3. Do the directors, participants of debt committee and fund manager have their own funds invested? A yes to this question does not provide a safe financial investment, it must offer some enhanced safety and security if assessed in combination with various other sensible financing plans.Is the MIC levered? The economic institution will certainly accept particular mortgages had by the MIC as security for a line of debt.

Last upgraded: Nov. 14, 2018 Few financial investments are as advantageous as a Home mortgage Financial Investment Company (MIC), when it concerns returns and tax obligation advantages. Because of their company structure, MICs do not pay income tax obligation and are legitimately mandated to disperse all of their revenues to financiers. MIC returns payouts are dealt with as interest earnings for tax objectives.

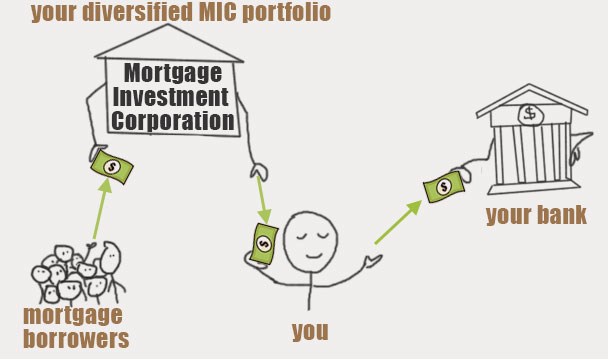

This does not suggest there are not threats, but, generally talking, whatever the wider stock exchange is doing, the Canadian actual estate market, particularly significant municipal areas like Toronto, Vancouver, and Montreal performs well. A MIC is a company created under the policies set out in the Earnings Tax Obligation Act, Area 130.1.

The MIC earns revenue from those mortgages on interest fees and general costs. The genuine appeal of a Home loan Financial Investment Firm is the return it provides investors compared to various other set earnings investments - Mortgage Investment Corporation. You will have no trouble locating a GIC that pays 2% for a 1 year term, as federal government bonds are equally as reduced

The smart Trick of Mortgage Investment Corporation That Nobody is Talking About

A MIC needs to be a Canadian company and it should spend its funds in home loans. That said, there are times when the MIC finishes up owning the mortgaged building due to foreclosure, sale contract, and so on.

MICs issue typical and preferred shares, issuing redeemable favored shares to investors with a taken care of dividend price. These shares are thought about to be "qualified financial investments" for deferred income strategies. This is perfect for capitalists that buy Home mortgage Investment Company shares via a self-directed authorized retirement savings strategy (RRSP), signed up retirement earnings additional info fund (RRIF), tax-free cost savings account (TFSA), deferred profit-sharing plan (DPSP), signed up education and learning savings strategy (RESP), or registered impairment cost savings strategy (RDSP)

3 Easy Facts About Mortgage Investment Corporation Described

And Deferred Plans do not pay any type of tax on the interest they are approximated to receive. That said, those who hold TFSAs and annuitants of RRSPs or RRIFs may be hit with specific charge taxes if the financial investment in the MIC is thought about to be a "banned investment" according to Canada's tax code.

They will certainly guarantee you have actually discovered a Mortgage Financial investment Corporation with "professional financial investment" status. If the MIC qualifies, it might be extremely official website valuable come tax obligation time because the MIC does not pay tax obligation on the passion revenue and neither does the Deferred Strategy. Extra generally, if the MIC fails to satisfy the demands laid out by the Earnings Tax Act, the MICs earnings will be tired before it gets distributed to shareholders, lowering returns considerably.

A lot of these dangers can be lessened though by talking with a tax obligation consultant and investment representative. FBC has actually functioned solely with Canadian little service proprietors, business owners, financiers, farm drivers, and independent contractors for over 65 years. Over that time, we have helped 10s of countless clients from across the nation prepare and submit their tax obligations.

The Best Strategy To Use For Mortgage Investment Corporation

It shows up both the real estate and stock markets in Canada are at all time highs At the same time yields on bonds and GICs are still near record lows. Also money is shedding its appeal since power and food rates have pushed the rising cost of living rate to a multi-year high.

If rate of interest rise, a MIC's return would certainly likewise raise because higher home loan prices suggest more revenue! Individuals that purchase a mortgage go to my blog investment firm do not own the genuine estate. MIC capitalists merely make cash from the enviable setting of being a lending institution! It's like peer to peer financing in the U.S., Estonia, or other parts of Europe, other than every loan in a MIC is protected by real estate.

Lots of difficult working Canadians who want to acquire a residence can not get home loans from typical financial institutions since perhaps they're self used, or do not have a well established credit background. Or perhaps they want a short-term finance to establish a big residential property or make some restorations. Banks often tend to neglect these potential borrowers due to the fact that self utilized Canadians do not have steady revenues.

Report this page